他們的地板,是我們的天花板

我在 2018 年夏天加入 Binance。底薪大概落在每月 12,000 到 15,000 人民幣,行情好的時候算它一千五百美金。故事講到這裡,如果你看過夠多這種文章,你會開始準備那個轉折:然後幣漲了,一切都不一樣了。

並沒有。我刻意把數字說精確,因為這整件事一旦照這類故事慣常的方式去四捨五入,就垮了。

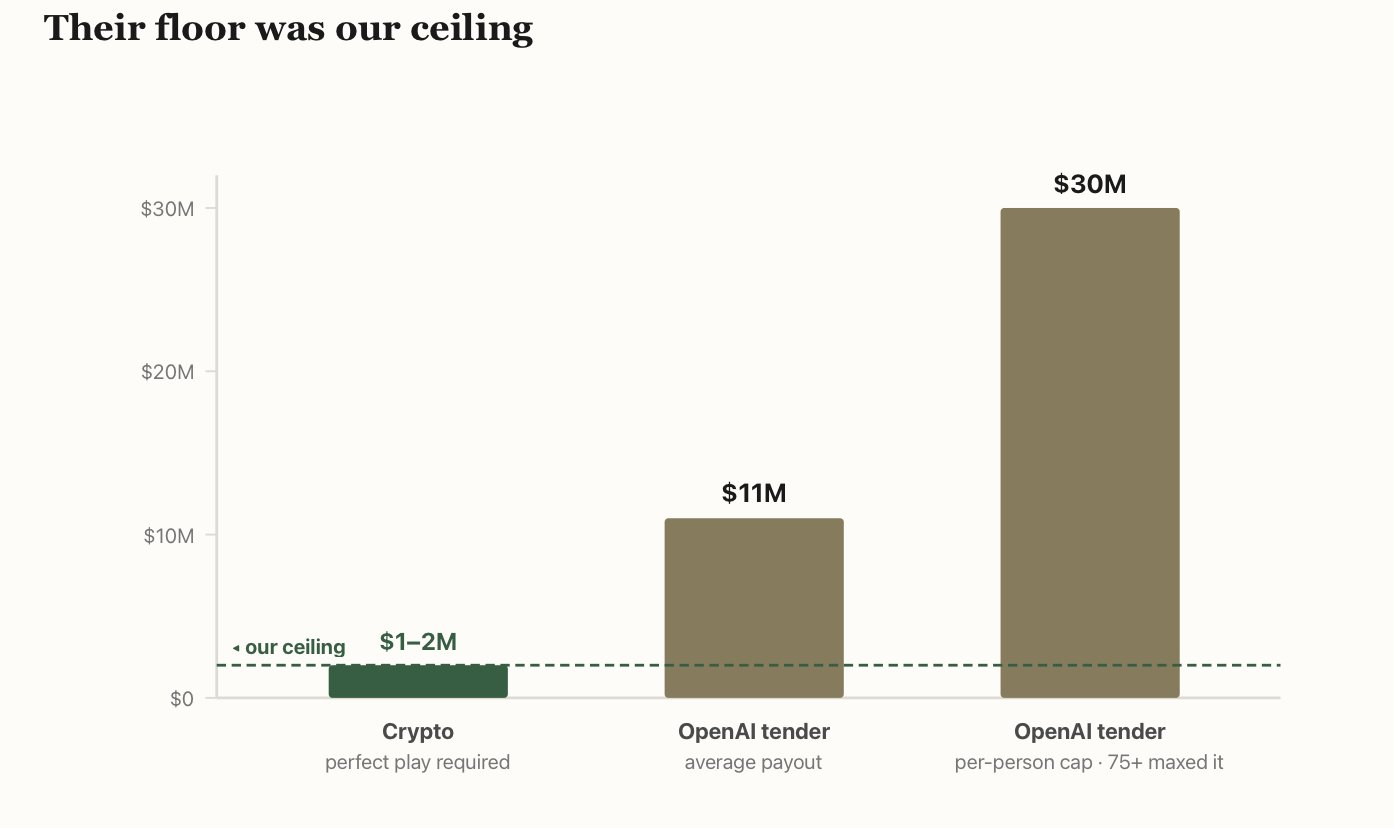

跟我一起算。它從來沒有一次算出來是更仁慈的。假設我從 2018 年開始,每個月把一半的薪水都丟進 BNB。假設我有那個胃,撐過每一次回撤都不賣,包括那些把大部分都吃回去的回撤,一路抱到 2021 年的頂。那樣的天花板——一個坐在我這個位子、把遊戲打到完美的人的最佳情況——大概是一到兩百萬美金。那不是小數目。在世界上大多數地方,那是一整段人生。我要你把這個數字記在腦子裡,因為它是一個天花板,而且要近乎完美的操作才搆得到。

現在把它擺在一個地板旁邊。2025 年 10 月,OpenAI 跑了一次內部 tender。六十五億美金,六百多名現任與前任員工,平均每人拿到大約一千一百萬。其中超過 75 人賣到了公司允許的上限,而上限是每人三千萬美金——這個 cap 還是 OpenAI 在外部投資人要求更多買入空間後,從一千萬翻了三倍上去的。沒有回撤要撐。沒有頂要抓。你把工作做了,股權累積了,然後一個公司自己辦的市場出現,把它換成現金。他們的地板,是一個我只能在試算表裡、靠後見之明加一副鐵打的胃才搆得到的數字。

crypto 打到完美:一個 $1–2M 的天花板,你還得抓得分毫不差——抱過每一次回撤直到 2021 年的頂。OpenAI 2025 年 10 月的 tender:平均 $11M,不需要任何一次看盤的判斷。連他們的平均,都遠遠高過我們的最佳情況。

crypto 打到完美:一個 $1–2M 的天花板,你還得抓得分毫不差——抱過每一次回撤直到 2021 年的頂。OpenAI 2025 年 10 月的 tender:平均 $11M,不需要任何一次看盤的判斷。連他們的平均,都遠遠高過我們的最佳情況。

他們的地板,是我們的天花板。

這個月有一條 thread 爆了,描述那個地板創造出來的世界。是 Deedy(@deedydas)寫的,值得一讀。他說,舊金山的氛圍很躁。一群大概一萬人的人,在幾年內就到了退休等級的財富,而這群人之外的每個人,都感覺到那扇門正在關上。他把其餘的人分成幾種一眼認得出來的群體:那些覺得自己畢生的技能突然不再重要的工程師;那些眼看著自己那一層被掏空、卻沒有人脈、履歷上也沒有 AI 的中層主管;還有那些已經上岸的人——其中一個跟他說,他不會賣掉自己的公司,因為一旦賣了,他就只剩下錢。我是用那種「讀到一段很準地說中你的話」的方式讀它的。他沒說錯,而且我不打算假裝他描述的那種焦慮跳過了我。它沒有。但我一直坐在隔壁那個產業,而從 crypto 這個位子看出去,同一幅畫面讀起來更糟——而且不是因為那條 thread 以為的原因。

那條 thread 把這個落差當成一件「發生在人身上」的事。時機、運氣、剛好在那個房間裡。我過去這兩年在做交易的技術盡職調查,以讀別人的 cap table 維生,而那種工作會毀掉你對「運氣論」的相信。你不再看到命運,你開始看到結構。我的天花板和他們的地板之間的落差,不是一個變數。是四個,疊起來,而且每一個都把下一個放大。

先從「誰擁有這個東西」開始。CZ 持有大概九成的 Binance。Sam Altman,眾所周知,有好幾年在 @OpenAI 沒有任何股權。這聽起來像是在講貪婪。不是。這是在講分配。當創辦人幾乎把一切都留著,那麼能流到 2018 年那個亞洲員工手上的上行空間,從結構上就是一個四捨五入的誤差。當創辦人持有的很少,其他所有人去分的那個股權池就很巨大,一個「早期但非創始」的員工,最後可能握著一份會印鈔的股份。同樣的成功,相反的分配,在任何人知道誰會贏之前好幾年,就決定了。

不是一個變數——是四個,疊起來,每一個都把下一個放大。我的天花板和他們的地板之間的落差,在我的職級之上、在我入職之前,就決定好了。

不是一個變數——是四個,疊起來,每一個都把下一個放大。我的天花板和他們的地板之間的落差,在我的職級之上、在我入職之前,就決定好了。

再來是他們付你的那個工具。我們拿到的,實際上是一個幣。一個幣沒有 vesting cliff 保護你不被自己害到,下跌的路上也沒有一個地板接住你。要靠它贏,你得做一次有規模的市場判斷,然後再做第二次判斷才真的出得了場,而大多數人兩次都沒做對。他們拿到的是有結構化 vesting 的股權。股權不要求你當一個交易員。它就只是待在那裡,在你做你的工作的同時複利,而最壞的情況通常還是一個正數。

再來是這一切坐落其上的那份薪水。我的底薪是上海底薪。他們的是舊金山底薪,在算進任何一股之前,就高了五到十倍。那個落差不只是生活品質的問題。高底薪,正是讓你能「抱著股權」而不是「賣掉它來過活」的東西——這意味著結構性的優勢,又把行為上的優勢複利了一次。最有本錢等待的人,正是最不需要等待的人。

然後是你怎麼變現的。我們是 DIY 式的流動性。你對著盤口,試圖在一個你猶豫的時候就能跌掉八成的資產裡抓一個出場時機。他們有的是公司辦的 tender。OpenAI 沒有要它的員工自己去找買家。它組織了買家、定了價格、設了上限,然後把錢匯過去。整件事裡最難的那一部分——把紙上的財富變成現金、又不把價格砸掉——對他們來說,是被當成一項福利處理掉的。

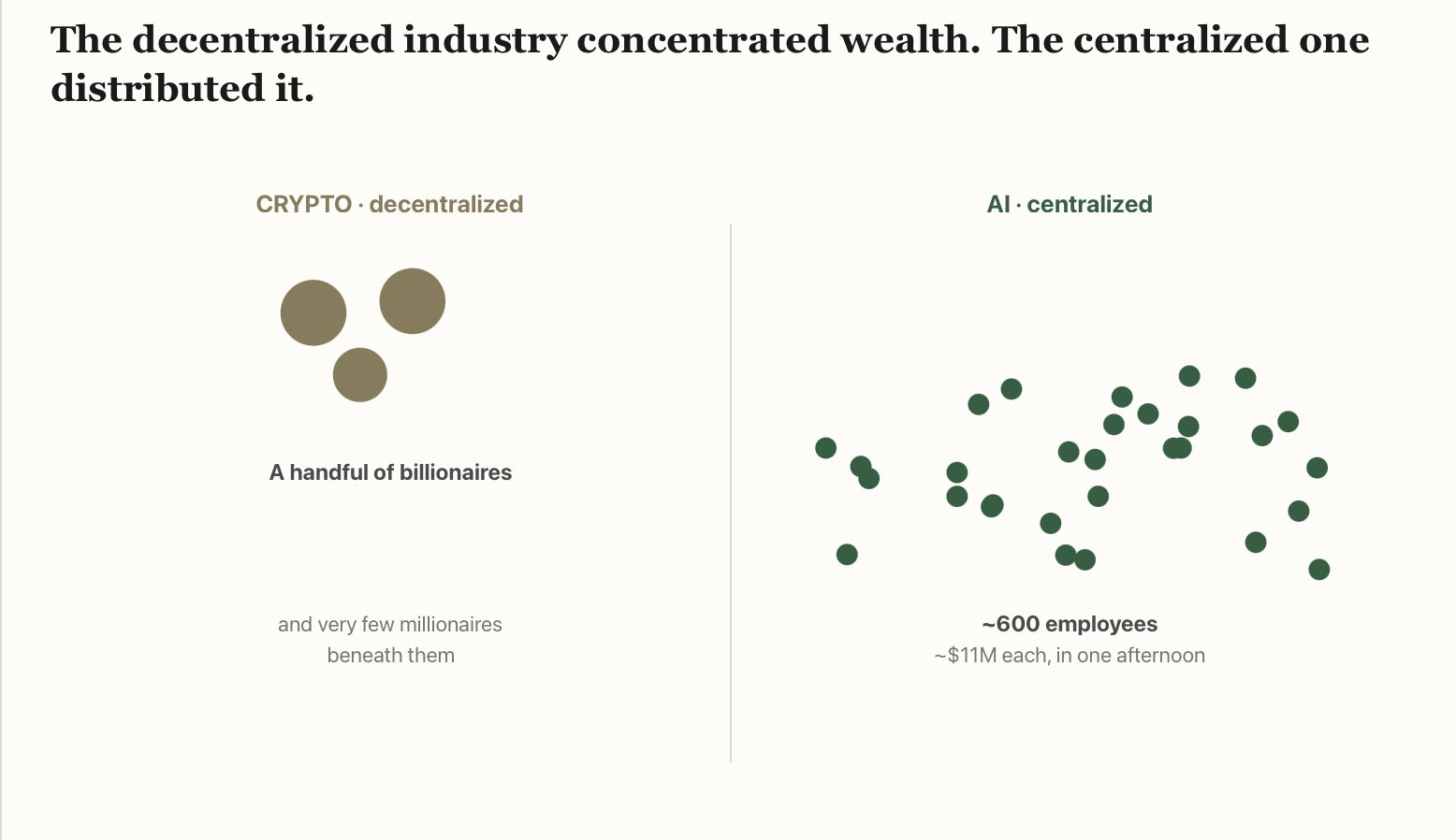

創辦人集中度、支付工具、薪資錨點、流動性機制。把它們乘起來,你會落在一個大多數人覺得反直覺的地方,而那也是我一直反覆在想的部分。crypto——這個整套說辭就是去中心化的產業——把財富集中得比幾乎所有在它之前的東西都更狠。它造出了一張很短的億萬富翁名單:CZ、Brian Armstrong、帳面巔峰時的 SBF,而他們底下的百萬富翁少之又少。AI——這個由少數幾家 lab 掌控的中心化產業——才是真正做到分配的那一個。六百人,平均一千一百萬,在一個下午之內。做到這個分配的東西不是一套意識形態。是一個結構化的內部市場,一段最無聊不過的金融管路,而它把比十年去中心化口號還要多的財富,移動到了比那更多的普通員工手上。我們被告知,那個無需信任的系統會把上行空間民主化。真正把它民主化的那個系統,有一張 cap table、一個 tender 管理員、以及一個因為需求太高而不得不往上調的三千萬美金上限。

crypto 整套說辭就是去中心化,而它把財富集中得比幾乎所有東西都更狠。AI,由少數幾家 lab 掌控,卻是真正把它分配出去的那個產業——透過一段最無聊不過的金融管路:一個結構化的內部市場。

crypto 整套說辭就是去中心化,而它把財富集中得比幾乎所有東西都更狠。AI,由少數幾家 lab 掌控,卻是真正把它分配出去的那個產業——透過一段最無聊不過的金融管路:一個結構化的內部市場。

我這裡沒有一個漂亮的結尾。這篇文章誠實的版本不會收束,因為我自己還沒收束。Greg Brockman(@gdb)這個月在法庭上作證,說他的 OpenAI 股份價值接近三百億美金,而當律師問他是不是「剛好」就富了三百億,他說薪酬相對於使命是次要的。我相信他,而這並沒有讓我好過。那些數學還是有些夜裡在我腦子裡跑——那個「一半薪水丟進 BNB」的數學,那個是他們的地板的、完美操作的天花板。

改變的不是焦慮。是焦慮的意義。有好幾年,它感覺像一個判決,好像那個數字是一個分數,而我的分數說我選錯了、坐錯了桌、是錯的那種聰明。讀夠多的 cap table 會把這種想法從你身上打掉。你會看見,那個落差是由四個結構性變數設定的,而它們在你的職級之上、在你入職之前就決定了——再怎麼早、再怎麼在我 2018 年那個位子上更拼,都彎不動它們。那不會讓你更有錢。它甚至不會剛好讓你更平靜。它只是讓那個數字,不再是關於你的。

Deedy 描述的那種躁動,是一萬個人把一個結構性的結果,讀成了一個關於自己的結果。我讀過那個結構了。我還是焦慮。我只是不再搞不清楚那是誰的判決——因為它從來就不是一個判決。它是一張 cap table,在我們任何人入座之前,就畫好了。

References

- OpenAI 2025-10 員工 tender — $6.6B · 600+ 人 · 平均約 $11M · 75+ 人賣到 $30M 上限 — finance.yahoo.com

- Greg Brockman 約 $30B 股份 +「使命優先」庭上證詞(Musk v. OpenAI,2026-05-04)— nbcnews.com

- CZ 持有約 90% Binance 股權 — dlnews.com

- Sam Altman 多年沒有 OpenAI 股權 — cnbc.com

- Deedy 的原始 thread — x.com/deedydas

Their floor was our ceiling

I joined Binance in the summer of 2018. Base pay was somewhere between 12,000 and 15,000 RMB a month, call it fifteen hundred US dollars on a good one. This is the point in the story where, if you have read enough of these, you brace for the turn: and then the token went up, and everything changed.

It did not. I am being exact about this on purpose, because the whole thing collapses if I round it the way these stories usually get rounded.

Do the math with me. It has never once come out kinder. Say I had put half of every paycheck into BNB, every month, starting in 2018. Say I had the stomach to hold through every drawdown without selling, including the ones that took most of it back, all the way to the 2021 top. The ceiling on that, the best case for someone in my seat playing the game perfectly, was roughly one to two million dollars. That is not nothing. In most of the world it is the whole arc of a life. I want that number sitting in your head, because it was a ceiling, and it cost near-perfect play to reach.

Now hold it next to a floor. In October 2025 OpenAI ran an internal tender. Six and a half billion dollars, more than 600 current and former employees, average payout around eleven million each. More than 75 of them sold the maximum the company allowed, and the maximum was thirty million dollars a person, a cap OpenAI had tripled from ten million after outside investors asked for more room to buy in. No drawdowns to stomach. No top to time. You did the work, the equity accrued, and a company-run market showed up to turn it into cash. Their floor was a number I could only reach in a spreadsheet with hindsight and a cast-iron gut.

Crypto, played perfectly: a $1–2M ceiling you had to time flawlessly — hold through every drawdown to the 2021 top. OpenAI's October 2025 tender: $11M on average, no market call required. Even their average towers over our best case.

Their floor was our ceiling.

This month a thread went viral describing the world that floor created. Deedy (@deedydas) wrote it, and it is worth reading. The vibes in San Francisco, he said, feel frenetic. A group of maybe ten thousand people have hit retirement-grade wealth in a few years, and everyone outside that group feels the door closing. He sorted the rest into the recognizable groups. The engineers who think their life's skill just stopped mattering. The middle managers watching their layer get hollowed out with no network and no AI on the resume. And the people who already made it, one of whom told him he would not sell his company because if he sold it he would only have the money. I read it the way you read something that is accurate about you. He is not wrong, and I am not going to pretend the anxiety he is describing skips me. It does not. But I have been sitting one industry over, and from the crypto seat the same picture reads worse, and not for the reason the thread thinks.

The thread treats the gap as a thing that happened to people. Timing, luck, being in the room. I spent the last couple of years running technical due diligence on deals, reading other people's cap tables for a living, and that work ruins you for the luck story. You stop seeing fortune and start seeing structure. The gap between my ceiling and their floor is not one variable. It is four, stacked, and each one multiplies the next.

Start with who owns the thing. CZ held something like ninety percent of Binance. Sam Altman, famously, held no equity in @OpenAI for years. That sounds like a point about greed. It is not. It is a point about distribution. When the founder keeps almost everything, the upside that reaches the 2018 hire in Asia is a rounding error by construction. When the founder holds little, the equity pool that everyone else divides is enormous, and an early-but-not-founding employee can end up holding a stake that prints. Same success, opposite distribution, decided years before anyone knew who won.

Not one variable — four, stacked, and each one multiplied the next. The gap between my ceiling and their floor was decided above my pay grade and before my start date.

Then the instrument they paid you in. We were paid, effectively, in a token. A token has no vesting cliff protecting you from yourself and no floor under you on the way down. To win with it you had to make a market call, in size, and then a second call to actually get out, and most people got neither right. They were paid in equity with structured vesting. Equity does not ask you to be a trader. It just sits there and compounds while you do your job, and the worst case is usually still a number.

Then the wage it all sat on top of. My base was a Shanghai base. Theirs was a San Francisco base, five to ten times higher before a single share is counted. That gap is not just lifestyle. The high base is what lets you hold the equity instead of selling it to live, which means the structural advantage compounds the behavioral one. The people best positioned to wait were the ones who least needed to.

And then how you got liquid. We had do-it-yourself liquidity. You against the order book, trying to time an exit in an asset that could fall eighty percent while you hesitated. They had a company-run tender. OpenAI did not make its people find a buyer. It organized the buyer, set the price, set the cap, and wired the money. The single hardest part of the whole thing, turning paper into cash without destroying the price, was handled for them as a benefit.

Founder concentration, the pay instrument, the wage anchor, the liquidity mechanism. Multiply them and you land somewhere most people find counterintuitive, and it is the part I cannot stop turning over. Crypto, the industry whose entire pitch was decentralization, concentrated wealth harder than almost anything before it. It minted a short list of billionaires, CZ, Brian Armstrong, SBF at the paper peak, and very few millionaires under them. AI, the centralized industry run by a handful of labs, is the one that actually distributed. Six hundred people, eleven million on average, in one afternoon. The thing that did the distributing was not an ideology. It was a structured internal market, the most boring possible piece of financial plumbing, and it moved more wealth to more ordinary employees than a decade of decentralization rhetoric ever did. We were told the trustless system would democratize the upside. The system that actually democratized it had a cap table, a tender administrator, and a thirty-million-dollar limit it had to raise because demand was too high.

Crypto's entire pitch was decentralization, and it concentrated wealth harder than almost anything before it. AI, run by a handful of labs, is the industry that actually distributed it — through the most boring possible piece of financial plumbing: a structured internal market.

I do not have the clean ending here. The honest version of this essay does not resolve, because I have not resolved it. Greg Brockman (@gdb) testified in court this month that his OpenAI stake is worth close to thirty billion dollars, and when the lawyer asked if he just happened to be thirty billion dollars richer, he said compensation was secondary to the mission. I believe him, and it does not help. The math still runs in my head some nights, the half-paycheck-into-BNB math, the perfect-play ceiling that was their floor.

What changed is not the anxiety. It is what the anxiety means. For years it felt like a verdict, like the number was a score and mine said I had chosen wrong, worked at the wrong desk, been the wrong kind of smart. Reading enough cap tables beats that out of you. You see that the gap was set by four structural variables that were decided above your pay grade and before your start date, and that no amount of being early or working harder at my seat in 2018 was going to bend them. That does not make you richer. It does not even make you calmer, exactly. It just stops the number from being about you.

The frenetic energy Deedy is describing is ten thousand people reading a structural outcome as a personal one. I have read the structure. I am still anxious. I am just no longer confused about whose verdict it is, because it was never a verdict. It was a cap table, drawn before any of us sat down.

References

- OpenAI 2025-10 employee tender — $6.6B · 600+ people · ~$11M average · 75+ hit the $30M cap — finance.yahoo.com

- Greg Brockman's ~$30B stake + "mission first" testimony (Musk v. OpenAI, 2026-05-04) — nbcnews.com

- CZ held ~90% of Binance equity — dlnews.com

- Sam Altman held no OpenAI equity for years — cnbc.com

- Deedy's original thread — x.com/deedydas